Despite the perceived macroeconomic slowdown, major pharma continues to invest heavily in next-generation gene therapy platforms. Capital is flowing toward programs that show operational growth, manufacturability, and a credible path to commercialization. Yet behind the headlines capital is returning, but only to companies that demonstrate credible paths to execution and scale.

An Industry Re-Accelerating

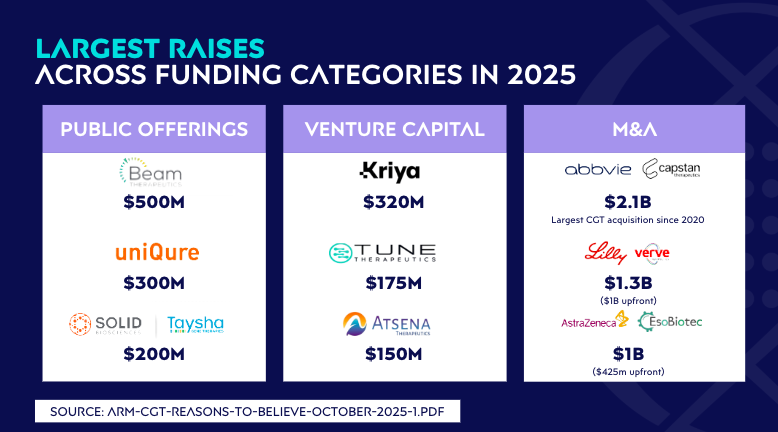

This year’s funding activity tells an important story. Public offerings, venture capital investments, and M&A deals all rebounded across the sector.

ARM reinforces this trend, with their recent report showing that cell and gene therapy companies are now outperforming the broader biotech market in 2025 after two challenging years. Investors are shifting away from backing single products and are instead directing capital toward platforms and therapeutic areas that can grow and scale.

A More Adaptive FDA Drives Momentum

One reason investors are returning is a more flexible and supportive regulatory environment. Earlier this year, the FDA removed REMS requirements for six CAR-T products, reducing administrative barriers and enabling care delivery outside of specialized academic centers. ARM notes that physicians expect this change to double CAR-T infusion rates due to lowered logistical burden. Meanwhile, accelerated approvals for CGTs continue to rise, with at least seven gene therapies potentially receiving accelerated approval between 2025 and 2027.

These milestones reduce uncertainty and shorten development timeline, but, they also raise expectations for manufacturing maturity, data integrity, and quality systems capable of supporting accelerated review.

Why Infrastructure Still Lags Behind Innovation

Even with renewed funding and regulatory support, manufacturing and supply chain capacity remain the biggest constraints for scale-up. ARM highlights that while scientific innovation is accelerating, the manufacturing and supply chain systems required to deliver these therapies are not keeping pace

Game-changing modalities like monoclonal antibodies show how long it can take for a promising technology to become a large, stable market. It took decades of investment in manufacturing, regulatory systems, and supply chain capacity to support their growth. Today, cell and gene therapies are on a similar path of early excitement, real challenges, and now a more grounded period of progress supported by stronger science and more mature business models.

Still, the bottlenecks are evident:

- Limited CGT GMP manufacturing capacity

- Fragile radiopharma isotope supply chains

- Undersized infrastructure needed to support growth of nuclear medicine

- Inadequate quality systems (paper-based, under-validated)

- Workforce shortages in CGT and radiopharma

- Increasing safety and data requirements for post-market surveillance

Execution Will Determine Who Wins the Next Growth Cycle

The companies securing capital today are the ones proving they can execute, not just innovate. In a market where capital is selective and regulatory expectations are tightening, companies must build:

- GMP-compliant facilities

- Mature quality infrastructure

- Reliable supply chain networks

- Validated manufacturing processes

- Scalable operational systems

The pace of scientific advancement is accelerating, yet the sector’s infrastructure continues to lag behind. Ensuring that new therapies reach patients will require coordinated progress in manufacturing, quality, supply chain, and regulatory readiness.

At Orchestra Life Sciences, we partner with innovators to transform regional momentum into real-world execution. OLS bridges engineering, quality, and regulatory execution to help companies move from discovery to delivery for our partners, clients, and community. We’re thrilled to be part of the solution to shape the next era of advanced therapy manufacturing.

Explore how the experts for the experts can help position your program for success: orchestralifesciences.com.